December and January have always been prime months for selling residential property in South Africa, and if you are a “Festive Season Seller”, here are two really important tips for you.

- Plan your finances

Understand and plan for all the financial implications, not just the legal ones.Prepare a cash-flow forecast so that you know what you will receive and when, and what you will have to pay and when. Your forecast will tell you what funds you must have available at all stages of the sale and transfer process, and it will answer your bottom-line question – what will be left in your pocket at the end of it all? - Don’t forget your CGT liability

There are many expenses you should provide for (ask your lawyer to help you list them), but in this article we’ll only address one of them – the CGT (Capital Gains Tax) aspect.

This is vital – if you made a “capital gain” on the sale (more on how to calculate that below) you could be liable to pay CGT. If so, it could well be a substantial liability, and not planning for it will leave you in a world of pain because if you can’t pay your tax bill SARS will be after you with a big stick (SARS has extensive powers when it comes to debt collection).

There is a bit of good news: The advantages of owning your own family home, and the value of property generally as an investment channel, will for most people outweigh the pain of having to pay tax when you eventually sell. Plus, as we shall see below, paying CGT on a property sale is not nearly as painful as it would be to pay income tax on it. Indeed, if the capital gain on your primary residence is R2m or less, your CGT bill is nil!

How does CGT on a property sale work?

This is a complex topic, so what follows is of necessity a summary of general principles only – there is no substitute for specific professional advice here!

- What is Capital Gains Tax? CGT forms part of your income tax and is a tax on any “capital gain” you make on an asset, in this case a property. The capital gain is the difference between your base cost and the proceeds of your sale.

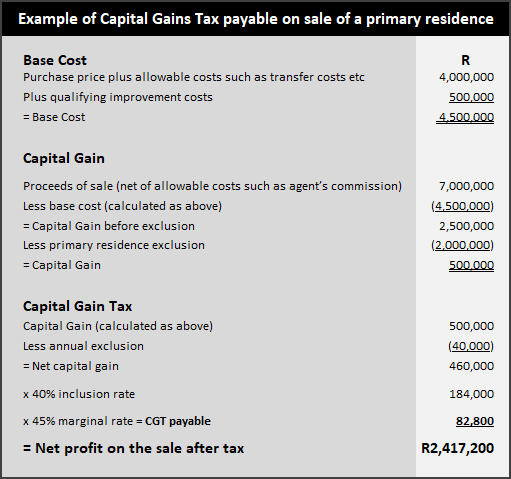

- What is “base cost”? This is what your property cost you to acquire (including transfer costs, transfer duty and the like) when you bought it. Note that CGT only kicked in on 1 October 2001, so if you bought the property before then it is the property’s value at that date that you will use. Qualifying improvement costs (extensions, additions and the like but excluding maintenance or repair costs) are also added to your base cost, so keep a separate note and proof of these as you incur them over the years. Our example calculation below assumes a homeowner who bought a number of years ago for R4m inclusive of transfer costs and duty, then spent a total of R500k on improvements (perhaps adding an extra room and a swimming pool).

- How do you calculate the “sale proceeds”? From the sale price you can deduct any costs of selling which are directly related to the sale, such as agent’s commission, advertising, legal costs and so on. In our example we assume net sale proceeds of R7m.

- How do you calculate the “capital gain”? This is the difference between the base cost and the proceeds of the sale (R2.5m in our example, before the primary residence exclusion).

- What can you deduct from the capital gain? If the property is in your personal name and is your “primary residence” (i.e., where you normally live) you can deduct a R2m exclusion from the capital gain. Note that if you used your house for business purposes or if you didn’t reside in it for the whole period of ownership, you need to take specific advice on how much (if any) of the exclusion is available to you. You can also deduct an “annual exclusion” of R40,000. In our example we assume the seller is entitled to both exclusions in full, resulting in a net capital gain of R460,000.

- How are you taxed on the net capital gain? The example below will help clarify this. Your capital gain is added to your annual income tax liability at the “inclusion rate” applicable to you. Individuals and special trusts have an inclusion rate of 40%, whereas other trusts and companies have an inclusion rate of 80%. You will then pay tax on that amount at your marginal tax rate (18% – 45% depending on your taxable income). In our example we assume an individual taxpayer paying tax at the highest marginal rate of 45%, the resulting tax liability of R82,800 amounting to just under 1.2% of the net sale proceeds. Our seller’s profit on the sale net of tax would then be R2,417,200.

So how much CGT will you actually pay?

For an individual your calculation is: Capital Gains Tax = Capital Gain x 40% inclusion rate x your marginal tax rate.

Have a look at the example below which assumes an individual home seller entitled to the full R2m primary residence exclusion and paying tax at the highest marginal tax rate of 45%. Then use your own figures and make your own calculation.

(Source: Adapted from SARS examples)

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNew